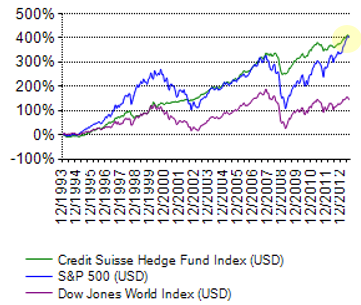

> Sliced democratizes access to hedge funds. Even though hedge funds have outperformed S&P 500 over the past decade, very few investors have access to them.

Hedge Funds on average do not outperform market indices such as S&P 500. I'm curious as to whether this was TechCrunch's take on the problem, or the startup's?

It can make sense to invest in hedge funds even if you don't expect your hedge fund portfolio to beat the market on average, if the hedge fund is uncorrelated with market returns. This is a basic result of Modern Portfolio Theory, but the intuition is that sometimes with the stock market down you will have better performance in your hedge funds (and vice versa), so your account will be less risky in the sense of having shallower troughs. If you want to take on the same risk (i.e. have troughs that are the same depth as if you just held stocks) you can invest more of your capital in stocks/hedge funds vs. bonds/cash, which means you are making better returns. It should be noted that the hedge fund universe is extremely broad, and different funds have different risk/return characteristics.

Venture capital is different because it is both correlated with market returns and the average fund significantly underperforms the market,[1] so getting good returns in venture capital is pretty much a question of getting allocations in the top 20 funds, which are persistently the best. They have the best returns in part because they have the best reputations and thus access to the deals that provide the highest returns (top entrepreneurs would take Andreesen Horowitz's money over money from Unknown Partners on the same terms).

I agree. I recall reading somewhere that warren buffet took a bet with a hedge fund guy a d his premise was also that a hedge fund cannot beat S&P index over a long term .

But a sucker is born every minute and I think sliced will do well for itself.

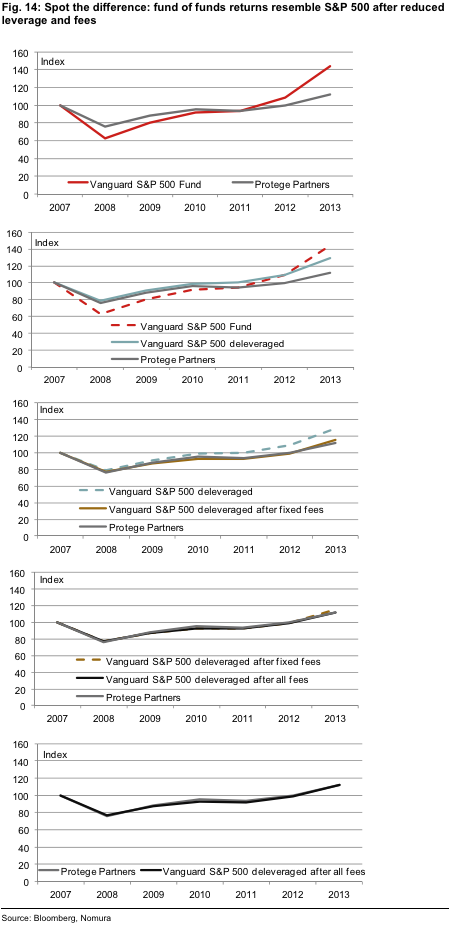

The bet between Warren Buffett and New York based asset manager Protégé Partners is that in the 10 years starting January 1, 2008 Protégé’s five hedge funds of funds will give a higher averaged returns to investors (after all fees) compared to Buffet's choice of the S&P index fund Vanguard Admiral. As of June 2014, Buffet's pick is up by 43.8% while Protégé is up only 12.5%.

It's mostly irrelevant. No one is investing in the hedge fund average, they are investing in the hedge funds that they think will do well. It's actually the same if you look at VC funds -- the overall returns of venture funds is poor, but the returns of the top quartile of funds is outstanding. In any case, the S&P 500 is not an appropriate benchmark for the hedge fund industry as a whole, because many hedge funds do not invest (solely) in equities and those that do theoretically have different risk characteristics from the market.

I think it is unlikely that hedge fund picking is possible for the following reasons. First, if a fund consistently produces outsized risk-adjusted returns the fund would increase their fees to capture most of those returns (Rentech, formerly Bridgewater). Second, a fund which has outsized risk adjusted returns net of fees would become very popular, receive more investment which creates a drag on returns until either the fund closes to new investors (Rentech) or returns reverted to the mean.

Funds frequently return capital or close to new money in order to stay below their investment capacity. Funds also sometimes charge less than the maximum they can get away with for various reasons. The premise of your argument is simply wrong. Moreover, you are ignoring the very real excess profits that are made on the way to this hypothetical equilibrium. Berkshire Hathaway shares aren't going to make you rich if you buy them today, but I'm guessing the people who bought them in 1970 don't care.

> Funds frequently return capital or close to new money in order to stay below their investment capacity.

The point is they are not open to investment once you have historical evidence that they are "good".

> Funds also sometimes charge less than the maximum they can get away with for various reasons.

The only reason I can think of is to increase investment. But that will happen even for minimal excess return.

> Moreover, you are ignoring the very real excess profits that are made on the way to this hypothetical equilibrium. Berkshire Hathaway shares aren't going to make you rich if you buy them today, but I'm guessing the people who bought them in 1970 don't care.

Obviously there are excess returns the question is if they can be reliably identified before hand and are accessible.

Are you invested in hedge funds? Which ones do you think are good now?

The cliche among hedge fund guys is to be "long term greedy" not "short term greedy", which explains why some funds try to be more investor friendly with fees. You also have flukes like Berkshire that seem to have undercharged simply out of benevolence. I don't really discuss my investments much, but I mostly do not invest in hedge funds for reasons of tax efficiency--a restriction that doesn't apply to many institutional investors. The one fund I am invested in has significantly outperformed with low risk during my holding period. The funds that I would invest in are small funds that probably no one here has heard of.

How do you suppose one tell which hedge fund will do better and which won't beforehand? Past performance? We know that's not a good indicator. If you can tell which hedge funds will do better in the future, you probably can tell which stocks will do better, and then why not just got it yourself without giving someone else 2 and 20?

We agree that S&P500 and hedge funds have different risk factors.

The point is that S&P500 is a lot less riskier and with better returns than an average hedge fund.

Investing in stocks is more labor-intensive than investing in funds. I can identify a few great managers that will do very well over time, write them a check, and be done. By your logic, why should anyone give YC or a16z money? I mean, if I know that YC is better at picking startups, why don't I just go pick my own startups? It's two different skillsets.

It's clearly not the case that I cannot select a set of hedge funds that is less risky than the S&P500. Fixed income funds, for example are much less risky (ignoring for argument's sake some details like inflation risk). I don't know if the "average" hedge fund is more or less risky than the S&P500. Depends how you define average. But no one is investing in the average, you couldn't do so even if you wanted to.

On the other side of the coin, there are index funds for fixed income too. That would be a better compare against hedge fund that primarily uses fixed income assets. (For hybrid hedge funds, there are hybrid index funds too.) Once again, the 2 and 20 payment structure makes it very hard for it to beat a 0.2 fee index fund.

And as for clearly better funds like A16Z and YC now, there have many numerous that have held that crown before. Fees and fund expansion have resulted in worse results -- allowing newer players like A16Z and YC to take off.

My argument is that I don't think it's clear who'll beat the broad market (for their asset class) once the fees are taken out. I suppose we disagree about the value of high-fee managed funds (whether VC, PE, Hedge, etc.). That's fine.

Anyway, enough digression from the discussion on hand.

Good luck to the founders in making their value proposition clear. I am sure there are lots of people want to invest in hedge funds but don't have the funds to invest directly. They will find this appealing.

I didn't say hedge funds shouldn't be benchmarked to their appropriate index, I said that hedge funds as a whole shouldn't be benchmarked to the S&P500 because they're not all equity funds. In fact, the majority of hedge fund allocated dollars are NOT invested in directional equity (not including strategies like merger arb that technically invest in equities but have totally different risk/reward from the market). It's not "the other side of the coin", it's my point exactly.

{kind=link}

{kind=link}

Hedge Funds on average do not outperform market indices such as S&P 500. I'm curious as to whether this was TechCrunch's take on the problem, or the startup's?